Earthbound: Global Airline Industry

April 14, 2020 | Expert Insights

Turbulence in the making

The International Air Transport Association (IATA), in 2019, announced a dip in the profit due to slowing demand and rise of fuel cost. The Boeing 737 Max disaster left hundreds of planes stranded on tarmacs or factory floors, resulting in the cancellation of thousands of flights and cancellation/ delay in aircraft orders. Alexander Juniac, IATA's Director General and CEO had issued a dire warning, "This year will be the tenth consecutive year in the black for the airline industry. But margins are being squeezed by rising costs right across the board—including labor, fuel, and infrastructure." He had not factored in the COVID-19 disaster waiting to strike.

Vectoring the virus

There is no doubt that the airline industry is culpable for the pace at which the "Black Swan" unfurled itself around the globe. While the contagion spread through human to human transmissions in China, scores of flights carrying thousands of unsuspecting passengers flew unchecked to almost every part of the globe. The World Health Organisation (WHO) vacillated in its decision to seek an international ban on flights out of China, exacerbating the situation. It is, therefore, not surprising that the COVID-19 has battered the airline industry. The industry faced threats after the 2011 terrorist attack in America. It took years for the industry to recover.

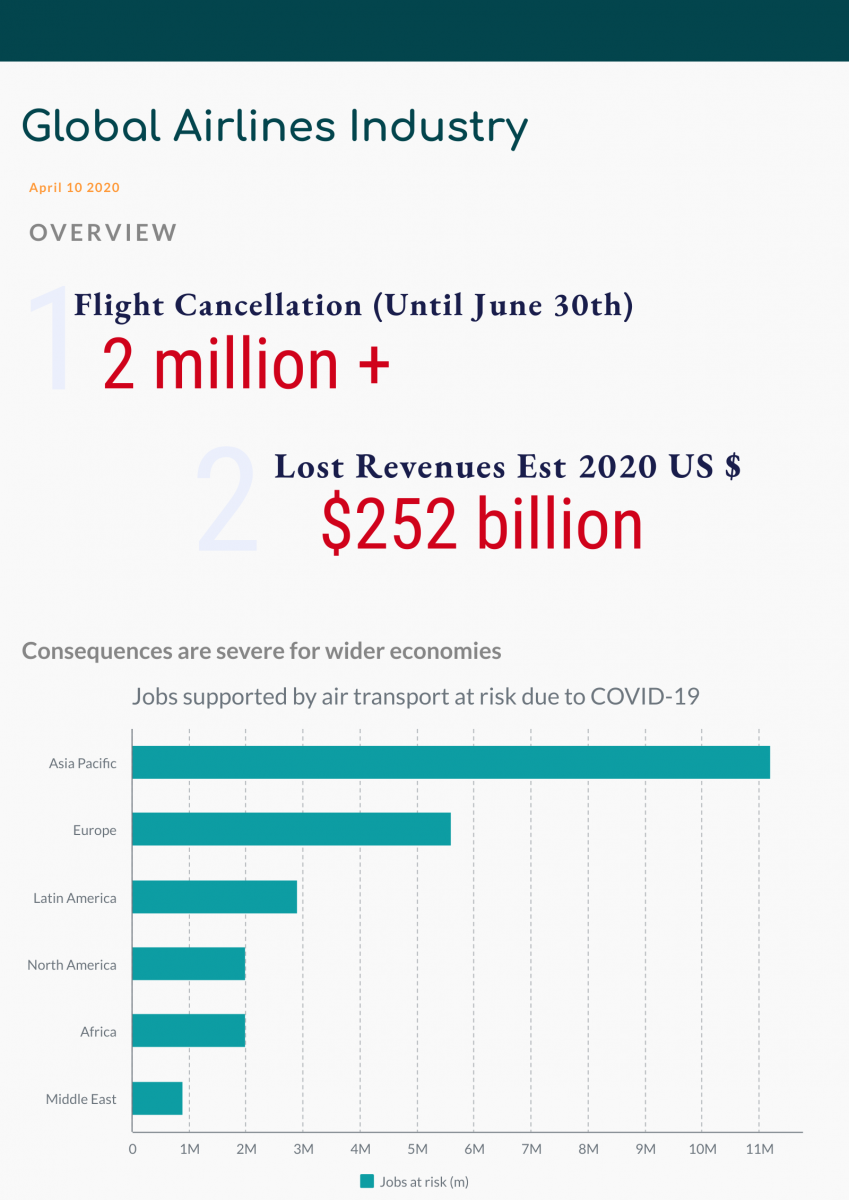

Industry pundits estimate a loss of $ 252 billion to the global commercial aviation sector for 2020.

At the start of 2020, a typical airline had two months of cash reserve. But, there is a high burn rate of about $61 billion in the second quarter. This is because most airlines expend their profits on stock buybacks to enrich investors, including their executives, whose positions often come with stock holding. An otherwise-solvent enterprise incapable of securing sufficient liquidity to cover its current operating costs can be forced into bankruptcy.

If aviation is not functioning, the economic damage goes far beyond the sector itself. The livelihood of 65.5 million people who are dependent on the industry, including sectors such as travel and tourism is at stake. IATA has calculated that 25 million jobs in the aviation and allied sectors are at risk across the world. Airlines are resorting to desperate cost-cutting measures to stay afloat; unpaid leave to staff, salary cuts across all levels of hierarchy, halting production on new aircraft and reviewing plans for airport expansions and closing down less profitable ones.

Leasing firms having access to capital, could repurchase planes from straitened airlines and then lease them back. But, widespread insolvencies flood the market with second-hand aircraft, further lowering charter rates could affect these firms. Aviation Insurance has also been affected because airplanes with a total insured value of more than $160 billion are grounded around the world.

If the status-quo extends, resuming the operation will become arduous as airworthiness certificates may no longer be valid, and airlines will require maintenance work.

Bare Indian skies

The Indian airline industry is in grave danger of insolvency. The industry contributed 1.5% to India's GDP, an economic contribution of $35 billion and supported 6.2 million jobs. Centre for Aviation (CAPA) estimates that the Indian airline industry including companies providing auxiliary services like airports and ground handlers could incur losses of between USD3.3 to 3.6 billion in the first fiscal quarter of 2020 ending June 30. IndiGo and SpiceJet will report losses of USD730 million and USD188 million if they are not revived by the end of June. CAPA also predicts that Tata Sons may have to consolidate holdings in its two airlines - Vistara and AirAsia India - and operate just one. Meanwhile, the government's plan to sell off its stake in Air India is likely to be delayed until after FY2021. On April 5, Air Deccan ceased all operations until further notice, and all its employees were being put on sabbatical without pay.

A silver lining

The industry's carbon-dioxide emissions between February 1 and March 19 fell by more than 10 million tons. The traffic forecasts by the IATA suggest airlines' emissions could drop as much as 38% in 2020. There are reports that the ozone layer is healing faster than before.

Assessment

- Aviation has become the sinews of international trade and other sectors. The industry cannot recover unless the commercial aviation business is dusted up and made to stand. The governments will have to step in, despite their host of other priorities, and support their early recovery.

- However, travel phobia out of fear of infection will keep most non-essential travellers grounded. This will be reflected in depressed bookings for the remaining part of this year. Hence, it will be a long, hard and painful road to recovery.

- Governments all around the world will not accept the risk of reinfection. After 9/11, although many new processes were imposed, it took the industry approximately 20 years to sort this out. Therefore, the airline industry must have dialogues on post- COVID-19 approaches to find predictable and efficient ways to manage travel. The goal we should have is an effective set of standard practices that can be implemented globally as required.

Author: Christina George(aka Bincy), Editor, Synergia Insights

Comments